Drone Insurance Guide: Make Sure You’re Covered

Drones are taking many industries by storm—from Hollywood cinematography and Midwest farming to Silicon Valley startups and New York City real estate tours.

Any savvy operator knows, with the thrill of flying come the real-world risks—technical glitches, unpredictable weather, and those occasional pilot mishaps.

That’s where understanding your drone insurance options becomes paramount.

This definitive guide is tailor-made for the American drone enthusiast, breaking down the ins and outs of drone insurance policies available in the United States.

Let us walk you through how to shield your drone with the right insurance so you are at peace each time you take your bird to the sky.

First things first, let’s try to understand the potential risks of flying a drone without insurance.

Potential Risks of Flying a Drone Without Insurance

Let’s face it. Life is unpredictable, and so are drones!

Flying drones come with its own share of risks. It can be an equipment malfunction, a crash into a powerline or tree, or maybe a flyaway.

Here are some potential risks of flying a drone without insurance:

- Property Damage: A drone might crash into buildings, vehicles, or other structures. Without insurance, the drone operator might have to pay out-of-pocket for repairs or replacements.

- Personal Injury: If a drone injures someone—whether due to malfunction, pilot error, or unforeseen circumstances—the operator could be liable for medical expenses, legal fees, and potentially other related costs.

- Malfunctioning Equipment: Over time, a drone’s components can wear out or malfunction, potentially leading to accidents. Without insurance, operators are entirely on their own for any resulting liabilities.

- Loss or Theft: Without insurance, you bear the full cost of replacing your drone if it’s lost or stolen.

- Third-party Claims: Without liability coverage, you’re at risk of facing potentially hefty out-of-pocket expenses if third parties (other than the drone owner/operator) claim damages or injuries caused by your drone.

- Contract Requirements: Most, if not all, contracts that you will work under as a drone pilot will have an insurance requirement. If you choose to fulfill the contract without the required insurance in place, you’re violating the terms which puts you and the client in jeopardy.

As you can imagine, you do not want to find yourself exposed if something unfortunate happens.

Like any other type of coverage, drone insurance mitigates risk by providing protection against possible bodily injury and property damage.

But which drone insurance should you choose? Let’s break it down.

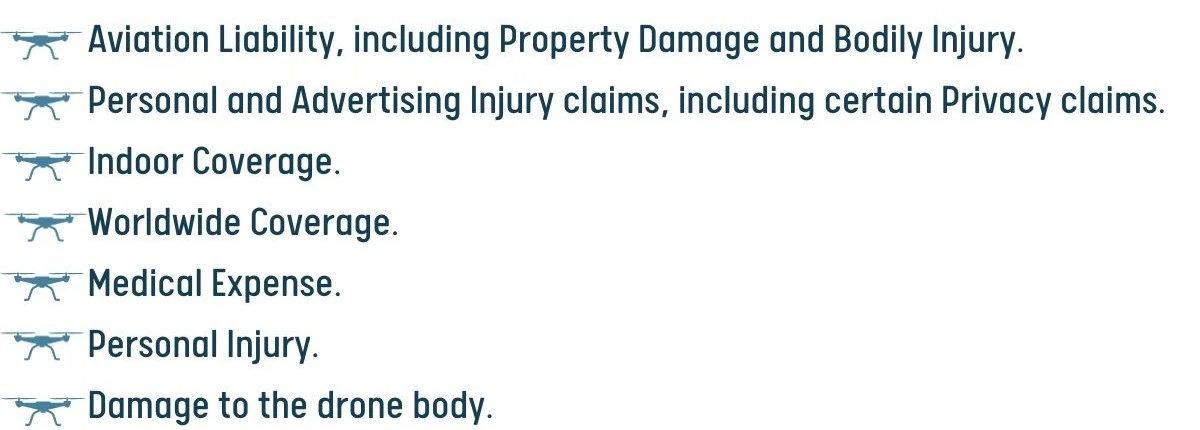

What Kind of Drone Insurance Coverage is Available?

Source: Skywatch

Source: Skywatch

Similar to other insurance types, drone insurance also provides a wide range of coverage areas.

Let’s take a look at some of them:

Hull Insurance

Hull insurance covers damage to the actual drone. Physical damage that affects your drone itself. If your drone crashes, malfunctions, or has an accident, this insurance can help with the repair or replacement costs. Keep in mind this does not cover the payloads – sensors, etc.

Liability Insurance

If your drone causes harm to other people or damages their property, this insurance will protect you from financial responsibility. This is especially important for commercial drone operators who fly in populated areas where the risk of injury or property damage is higher.

Payload Insurance

If you have special equipment like cameras or sensors attached to your drone, this insurance will cover them in case they get damaged or lost. This is generally not automatically included and therefore you’ll need to ensure any payloads you want covered are noted in your policy.

Ground Equipment Insurance

This insurance covers the equipment you use on the ground to control your drone, like extra remote control, base stations, cameras, and any other equipment you add to your policy.

Personal Injury Insurance

If your drone operations cause harm to someone’s reputation or rights, this insurance can help you handle legal issues related to that.

Non-Owned Coverage

If you rent or borrow a drone instead of owning one, this insurance provides liability protection in case of accidents.

Data Protection and Cyber Liability Insurance

This insurance covers damages resulting from data breaches or cyber-attacks on your drone’s software or the data it collects.

Before choosing a drone insurance policy, consider what kind of coverage you need based on how you use your drone. For example, if you own a business, you must look for drone business insurance that provides extensive coverage.

As always, policies and coverage can vary from provider to provider, so it’s recommended to compare options. You can also talk to an insurance agent or attorney who knows about UAV insurance to help you with the process.

How Much Does Drone Insurance Cost?

The cost of drone insurance varies significantly depending on several factors, including:

- Type of coverage

- Amount of liability coverage selected

- Value of the drone and related ancillary equipment including in the policy

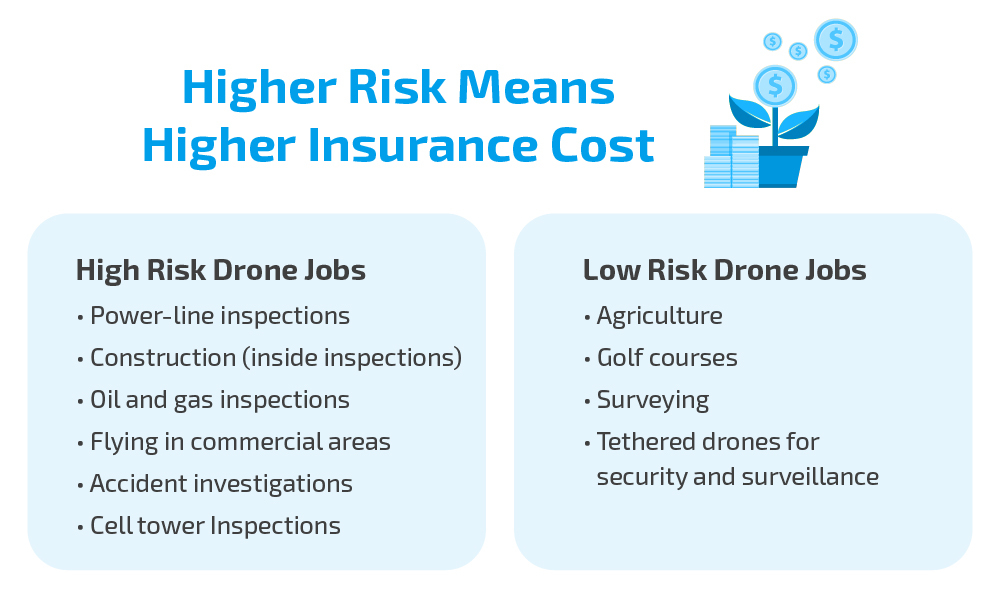

- Purpose for which the drone is being used (for example – basic marketing videos vs inspections of complex infrastructure assets

- Pilot experience

- Geographical location where the drone will be flown.

Liability Insurance

Drone liability insurance is usually the most expensive insurance. It can start from $500 to $1,000 per year for $500,000 to $1 million coverage, but it may go up if your drone operations are considered riskier.

Clients such as large production houses and big construction companies may even ask drone pilots to buy coverage with a $5 million CSL (Combined Single Limit).

Combined Single Limit is the total of bodily injury liability coverage and property damage liability coverage.

Hull Insurance

It is often around 8-10% of your drone’s value per year. For example, if your drone is worth $1,500, hull insurance might cost around $120 to $150 per year.

Invasion of Privacy, Personal Injury, and Cyber Liability Insurance can be added to a drone liability policy, but the cost depends on the insurance company and the specifics of your drone use.

On-Demand Insurance

Some companies offer insurance that you can use only for specific flights. The cost can start at $10 per hour and can go higher depending on the details of the flight and drone.

Insurance companies are prone to considering the depreciated value and not the actual market value when settling a claim. So, avoid inflating your drone value when buying insurance.

Typically, liability-only drone insurance cost for coverage of $1 million is around $650. The cost of Hull insurance will amount to 10% of the cost of the drone. So, if you are flying a $1,000 Autel Evo, liability + hull insurance cost will be around $750.

Your UAV insurance cost will further increase if you opt for any add-ons like ground equipment coverage and payload coverage. We strongly recommend purchasing a higher drone liability insurance if you are taking on risky drone jobs.

How Can You Save on Your Drone Insurance Cost?

First, insurance is negotiable. So do not be afraid to haggle. After all, a penny saved is a penny earned. Secondly, your experience and training will be taken into account. Remember, your insurance policy is reviewed by an underwriter.

If you have a long, accident-free flying history and have undergone drone training from an organization of repute, these factors will work in your favor. Your drone crash insurance cost also depends on the nature of the jobs and the associated risk.

So, if you are using your drone for agricultural mapping, your insurance cost is likely to be lower compared to someone who is flying in areas of heavy interference.

Next, if you are an established player with a fleet of drones, you are likely to be offered a better deal. Your per-unit drone crash insurance cost is likely to be lower.

Also, for extremely small damages, it is not worthwhile putting in a claim. Typically, deductibles are pegged at 5% of the insured value. So, for small damages, it would be financially prudent to bear the cost yourself. Moreover, the lower number of claims filed will result in lower insurance costs too.

Finally, do not hide any information from your broker in a bid to get lower coverage. This is a strict no.

Last but not the least, you can get an education rate on your Skywatch insurance and save up to 15% by taking our Flight Mastery Training. This, coupled with a good Skywatch safety score, can push up your total discounts to as high as 30%.

Validity Periods of Drone Insurance Policy

Source: Skywatch

Source: Skywatch

It’s important to know how long your policy will be valid before you buy it. Generally, UAV insurance policies are offered for specific durations, such as:

Short-Term Policies

These policies might cover your drone for a single flight or a limited period, such as a day, a week, or a month. These policies are often used by individuals or businesses that need coverage for a specific event, project, or short-term activity.

Annual Policies

Many insurance companies offer annual policies that provide coverage for an entire year. These policies are suitable for drone operators who fly their drones regularly and want continuous coverage without the need to purchase insurance for each flight.

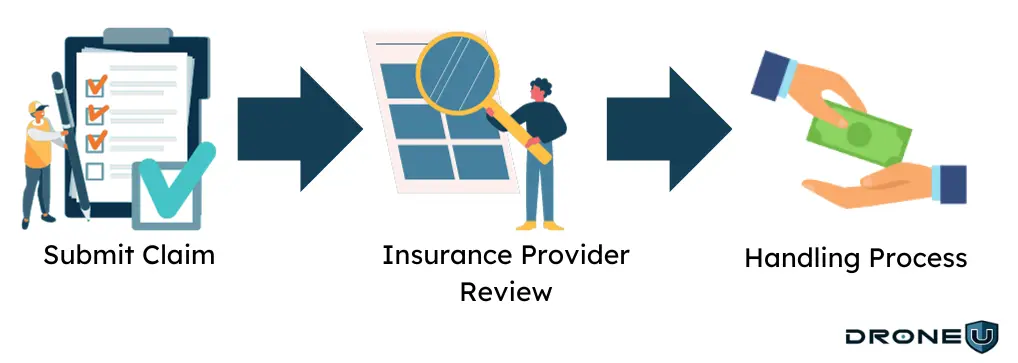

How to File a Drone Insurance Claim

In the unfortunate event of an accident or damage involving your drone, knowing how to file a drone insurance claim is crucial.

Before filing a claim, review your insurance policy to understand the coverage limits, deductibles, and any specific procedures the company requires for claims.

To start the claim process, you will need to contact your insurance provider and inform them of the incident. They will guide you through the necessary steps to submit a claim.

If your policy is a drone replacement insurance policy like StateFarm, the drone insurance claims process is relatively straightforward –

Step 1: You can file a claim via phone, online, or through an insurance agent.

Step 2: Your insurance provider will review the claim and might request additional information from you.

Step 3: Once your claim is assessed, your provider will share their estimate, and repair options, if applicable.

Step 4: If your claim is cleared, payments are sent out via wire transfer or mail.

However, if your drone crash caused damage to people or property, you will have to file a general liability insurance claim. This is a more complex process that requires additional documentation.

It’s essential to report drone-related incidents promptly to your insurance provider, even if you are unsure whether a claim will be necessary.

Here are some things to remember while doing so –

- Get the names, addresses, and phone numbers of everyone involved.

- Police reports, and any other documentation that is relevant to the claim.

- Do not discuss or share documents relevant to the claim with anyone in question.

- Photograph or video the scene, especially the damage to your drone and any property it may have damaged.

- Note down details of the accident, including weather conditions, exact date, location, and time of the incident, and any potential witnesses.

Top Drone Insurance Providers

In the vast market of drone insurance providers, each company has its unique strengths and specialties. Here is a quick comparison of top drone insurance companies so you can make an informed decision.

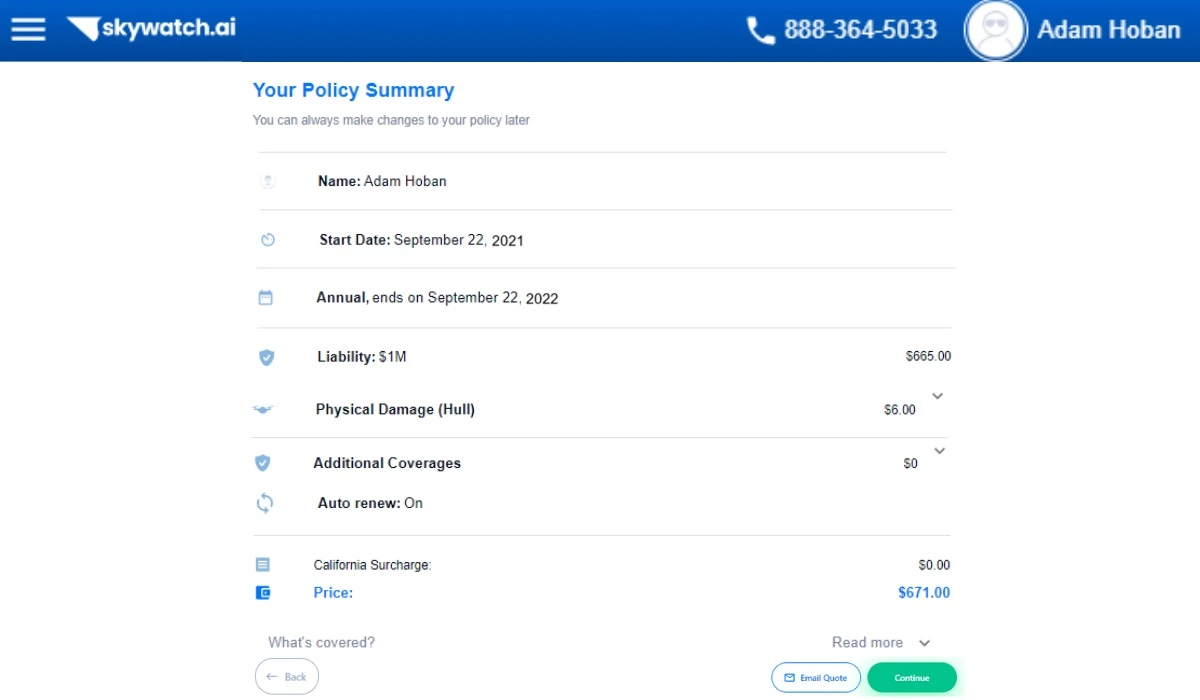

SkyWatch

SkyWatch.AI offers insurance policies that you can customize based on what you need. You can choose how much coverage you want for liability, damage to your drone (hull), and third-party property damage coverage.

This drone insurance policy also has an option where you can get insurance only for the hours you fly your drone.

Their app uses a Safety Score system to give you feedback on how safe your flights are. If you are a safe pilot, you might even get a discount on your insurance premium.

Enroll in our ‘Don’t Crash Course’ to become a safer pilot and save money on insurance policy.

Verifly (now Thimble)

Verifly, now known as Thimble, offers on-demand insurance. You can get coverage for just an hour, a whole day, or even a month. You can even buy insurance up to six months in advance.

Thimble is a popular provider of drone insurance for hobbyists and small businesses. The company offers liability coverage, hull coverage, and third-party property damage coverage.

DroneInsurance.com

DroneInsurance.com offers an array of flexible and customizable insurance plans that you can tailor to your needs. You can also add on-demand insurance, which gives you the flexibility to choose how much coverage you want and when you need it.

If your drone has special equipment, like cameras or sensors, you can add extra coverage for that.

DroneInsurance.com also offers protection for the ground equipment. They provide basic coverage that protects you during ground operations, and you can choose how much coverage you want based on what you need and how much you can afford.

Bullock Agency, Inc.

Bullock Agency has been a trusted insurance company for more than 30 years. They are experts in aviation insurance and offer different types of drone insurance policies to both businesses and individuals.

One of the great things about getting drone insurance from Bullock Agency is that they have a team of experienced professionals who know all about drone insurance. They can guide you to identify the perfect drone insurance policy that fits your needs.

Avion Insurance

Avion Insurance is a well-known company with a long history of insuring aircraft. They understand the potential risks that come with drones. Avion’s UAV insurance policies offer coverage for both liability and physical damage. Their policies are also customizable, so you can choose the coverage that best meets your needs.

State Farm Drone Insurance

State Farm Drone Insurance Policy is like a protection plan for your drone. It covers your drone if it gets stolen, accidentally damaged, or faces certain dangers. It is one of the best recreational drone insurance.

If your drone suffers physical damage or goes missing because of an accident or theft, you can ask State Farm for help. The good thing is that it’s reasonably priced, and in most cases, you won’t have to pay any deductibles. Isn’t that cool?

Check out our comprehensive State Farm Insurance Review to learn more.

Global Aerospace

Global Aerospace Drone Insurance is a comprehensive policy that includes damage to the drone, liability for any harm caused to others, and even the risk of invasion of privacy.

They also provide coverage for non-owned drones. The insurance is quite inclusive, safeguarding against third-party liability, damage to the drone, its contents, and related equipment, as well as privacy invasion and medical expenses.

The best part is – there is no annual deductible, so your coverage starts right away. This insurance is available for both recreational and commercial drone users.

Which is the Best Drone Insurance For You?

![]()

Choosing the right drone insurance depends on multiple factors including the kind of flying you do, the value of your equipment, and the potential risks you face.

Here’s a step-by-step guide to help you pick the best drone insurance for your needs:

Determine Your Needs

When picking UAV insurance in the U.S., identify if you’re flying for fun or business—commercial pilots often need beefier coverage. Make sure your policy fully covers your drone and any gear.

How often you fly also matters: if you’re an occasional flier, think short-term insurance; frequent fliers should lean toward long-term plans. If you’re jetting off abroad, double-check that your coverage goes international. And remember, flying downtown versus out in the country can come with its own set of risks, so pick accordingly.

Types of Coverage

We touched upon this topic earlier in this article. You need to be aware of the options available in the market, such as liability insurance, hull insurance, and ground equipment insurance. This knowledge will help you pick the best one for your needs.

Note: Most policies will have exclusions. Make sure you are aware of what isn’t covered.

Shop Around

When you’re on the hunt for UAV insurance, don’t just jump on the first deal that comes your way. Always play the field by getting multiple quotes—different providers often have their own spins on rates and what they’ll cover. While you’re comparing, it’s a smart move to find out reviews and see what folks are saying about a provider. This is your inside scoop on how they handle things, especially when the chips are down and you need to make a claim.

Understand what you’re signing up for, check what’s covered, and keep an eye out for any sneaky costs or conditions. Doing your homework now can save you a whole lot of headaches later.

Our Pick

We, at Drone U, have switched over to Skywatch from Global Aerospace over the last year. Skywatch’s parent company, Starr Insurance Companies has stellar credentials and was a practical solution to a large fleet.

With its unique discounting mechanism that encourages pilots to fly safely, we think that Skywatch drone insurance might be the best drone insurance for you.

With more than 100 years of experience in the insurance sector, Starr Insurance has a presence spanning five continents. Starr’s insurance company subsidiaries domiciled in the U.S., Bermuda, China, Hong Kong, Singapore, and the U.K. each have an A.M. Best rating of “A” (Excellent). Starr’s Lloyd’s syndicate has a Standard & Poor’s rating of “A+” (Strong).

Conclusion

Whether you’re flying drones as a hobby or for work, getting drone insurance is a smart move.

When choosing UAV insurance, think about what coverage you need based on how you use the drone, your experience, and how much the insurance costs.

Liability coverage is important to cover legal claims and costs if your drone causes accidents. Physical damage coverage protects your drone if it gets damaged in a crash or collision.

If you follow safe flying rules, keep detailed flight records, and get proper safety training, you might be able to get lower insurance costs.

One of the best ways to hone your skills and fly safely is to attend our flight mastery in-person training. This training will help you become a safe and confident drone pilot. Click here to learn more about our Flight Mastery training.

Frequently Asked Questions

1. Is it mandatory to get Insurance?

Certain states have made insurance mandatory for commercial pilots. Whereas, in other states, Part 107 pilots can still fly legally without purchasing insurance.

So should you fly without insurance? No!

If a drone flown by an uninsured pilot causes bodily harm or property damage, all of the financial liability will fall on the pilot. By not getting insurance, a pilot risks losing all his assets.

Brett Woods, a professional Part 107 pilot lost control of his drone and flew into a building through a window on the 27th floor. Luckily for Brett, the floor was unoccupied, and while the property was damaged, no one was injured. Brett’s insurance made good this damage.

Remember – If you are buying commercial on-demand insurance, your provider assumes that you have a Part 107 certification. However, you CANNOT claim damages without a valid Part 107 certificate. Certainly, another strong reason to get your Part 107 license.

2. Are UAVs covered by Homeowners Insurance?

Not if you are a Part 107 pilot. Part 107 pilots will have to purchase a separate insurance policy. But, if you are a hobby pilot, your drone might be covered under your homeowner’s insurance. However, we strongly recommend that you check the exact nature of coverage with your insurance provider.

3. Does insurance for drones cover theft?

Some drone insurance policies may include coverage for theft or loss of your drone. It’s essential to review the policy details to confirm this coverage.

4. Can I get insurance for my recreational drone?

Yes, recreational drone insurance is available to protect your drone from damage and provide liability coverage.

5. Does drone insurance cover damage caused by the drone to someone else’s property?

Yes, it typically includes liability coverage, which protects you if your drone causes damage to someone else’s property.

6. What factors affect drone insurance premiums?

UAV insurance premiums can be influenced by factors such as the type of coverage, UAV specifications, operator experience, and flying history.

7. Why should you choose Admitted Insurance Carriers?

An admitted insurance carrier, we learned has been approved by the state’s insurance department. Is this important? Yes!!!

Two BIG Reasons to Purchase Insurance from an Admitted Insurance Carrier:

Reason No. 1 – The State Acts as a Regulator

An Admitted Insurance Carrier must comply with all state insurance regulations. That means that Skywatch and Verifly (Thimble) need the state’s approval before increasing insurance premiums. However, Droneinsurance.com, a non-admitted insurance carrier is under no such obligation.

Reason No. 2 – You get Added Protection

If an Admitted Insurance Carrier goes bankrupt, the state steps in to honor all claims. So coverage from an admitted insurance carrier comes with added protection and ensures peace of mind.

YOU MAY ALSO LIKE...

Add Your Comment

Some of our most popular topics...

Top 10 Blogs

- 1. Autel Evo 2 vs DJI Mavic 3 – Which Drone Should You Buy in 2020?

- 2. Part 107 License FAQ | Your Drone Certificate Questions Answered

- 3. Flying Large Drones Over 55 Pounds Using Section 333 Exemption

- 4. Drone Insurance FAQ's – How to Get the Best and Most Affordable Coverage

- 5. LAANC Apps - Using Kittyhawk and Skyward for Approval

- 6. FAADroneZone - How to Apply for a Part 107 Waiver

- 7. Little Known Facts About Part 107’s “Visual Line of Sight (VLOS)" Rule That You Might Not Be Aware Of

- 8. Should You Get Drone Jobs through Drone Base?

- 9. Flying Drones Over Streets and Moving Traffic

- 10. Best Drones for Flying in the Wind

Top 10 Podcasts

- 1. What should I know about drone insurance?

- 2. BONUS EPISODE: Michael Singer v. City of Newton (City Drone Ordinance Nullified!)

- 3. Is there a place for me in the real estate industry if I lack photography and video skills?

- 4. Is the DJI Spark a good drone?

- 5. INTERVIEW WITH ANDY LUTEN

- 6. How to market your drone business

- 7. DJI Drone Comparison | DJI Phantom 4 Pro, Inspire 1, Inspire 2

- 8. Can I fly my drone over people if I have their consent?

- 9. Drone Photography Pricing for land-only drone jobs

- 10. Can I fly my drone over a road?

Download our No #1 Resource: Part 107 Study Guide

What's Inside this Guide?

- 2500+ pages of FAA material broken into digestible easy to read 279 pages

- Includes over 350 sample quiz & test questions(with answer keys)